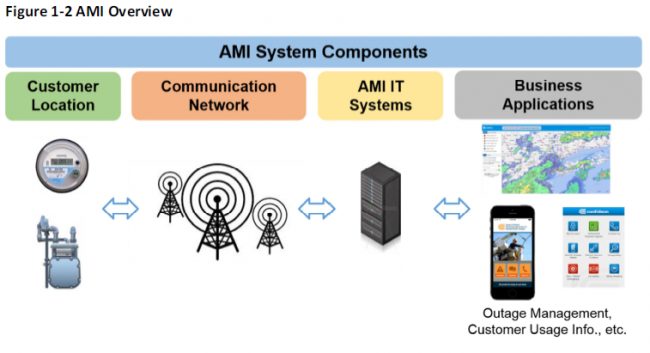

Growing use and falling costs of local distributed energy resources (DERs) and interactive, two-way information and communications technologies – smart meters, associated grid infrastructure, utility-customer demand response (DR) programs and cloud-based connected home, business and building energy management apps and services – is leading to a wholesale shift in the way we produce, distribute and consume energy.

![]() Faced with a fluid, fast-changing technological, business and regulatory environment, leading US utilities are increasingly developing innovative new strategic business and operating models in a bid to capitalize on these and other innovative digital energy and distributed energy resource management (DERM) technologies. They’re doing so in lieu of pursuing the traditional utility industry approach, which entails gaining regulatory approval to pass costs of investing in and rolling out new power lines and associated grid infrastructure – transformers, substations, etc. – when it comes time to replace aging grid infrastructure or demand for electricity in any one or more service areas approaches full capacity.

Faced with a fluid, fast-changing technological, business and regulatory environment, leading US utilities are increasingly developing innovative new strategic business and operating models in a bid to capitalize on these and other innovative digital energy and distributed energy resource management (DERM) technologies. They’re doing so in lieu of pursuing the traditional utility industry approach, which entails gaining regulatory approval to pass costs of investing in and rolling out new power lines and associated grid infrastructure – transformers, substations, etc. – when it comes time to replace aging grid infrastructure or demand for electricity in any one or more service areas approaches full capacity.

The trend has given rise to the term “non-wires alternatives” (NWAs) – DERs and digital energy grid services and management assets that hold out the promise of lowering costs, enhancing existing and opening up opportunities for new, interactive utility-customer grid products and services. Navigant Research highlights the trend in a new market research report.

Con Edison and the Digital Energy Grid

Significant from local, national, regional and global perspectives, growing use of non-wires alternatives is considered a trend capable of providing substantial additional impetus to the fast-growing use of distributed renewable and low-emissions energy resources. In turn, that would help avoid and adapt to the effects of climate change and stem the rising tide of ecosystems and services degradation and help fulfill local, national and global climate change and renewable goals.

Regulated, investor-owned utility (IOU) Consolidated Edison operates the New York City metropolitan area’s two predominant transmission and distribution (T&D) utilities. Combining the latest proven new energy and power technologies, its Con Edison (ConEd) subsidiary is in the midst of an ambitious grid-wide systems overhaul that, if successful, would deliver modern, 21st-century digital energy grid services throughout the New York City metro area.

Broadly speaking, Con Edison’s grid modernization entails making substantial, long-term investments in and capitalizing on the use of the latest software and ICT, intelligent grid-edge and distributed renewable and low-emissions grid assets, and engaging customers to participate in “behind the meter” distributed grid management solutions.

A live Utility-Neighborhood Demand Respond Management field test

ConEd’s Brooklyn-Queens Neighborhood Management Program (BQNMP) provides an apt illustration. Working with a variety of third-party specialists, including Oracle Utilities, Silver Springs Networks and a variety of customer demand-response program aggregators, ConEd is stepping up their use of innovative customer-sited and grid-edge DERs to realize the utility’s, as well as broader-based, grid transformation, clean energy and climate change action plans.

Faced with surging energy demand within its Brooklyn-Queens service territory, ConEd opted to invest in DERs and utility-customer DRM programs rather than taking its traditional approach to resolving the issue. ConEd’s VP of Distributed Energy Integration Matt Ketschke explained in an interview.

ConEd would have invested over $1 billion over a 20-year time horizon to build a new substation had it followed the conventional utility approach to resolve the issue by boosting its capacity to provide electricity service across the area. It expects to achieve the same set of goals by rolling out an evolving mix of new DR programs and DERs at lower cost and much faster.

NWA, DERs and DRM

ConEd’s investments in and ambitious expectations regarding DERs and DRM programs, products and services is part and parcel of a nationwide trend.

“[G]rid management and distributed energy resources (DER) technologies have improved, utilities are looking to engage customers more and provide more value-added services, and policy concerns related to cost and the environment have grown,” the authors of Navigant Research’s, “Non-Wires Alternatives Non-Traditional Transmission and Distribution Solutions: Market Drivers and Barriers, Business Models, and Global Market Forecasts.”

“In reaction, more creative solutions are being explored to address infrastructure needs at a lower cost with greater customer and environmental benefits. These types of projects are known as non-wires alternatives (NWAs).”

NWA Market Barriers

Navigant’s research team goes on to highlight the market barriers utilities and NWA value chain participants face in seeing their projects and plans through to fruition:

- Lack of regulatory incentives: If there is no regulatory pressure in place, there are few reasons why the utility would adopt a NWA. There is a higher perceived risk associated with these types of short measure life projects compared to a traditional upgrade that is built to last 20 years or more. In addition, a T&D upgrade aligns with the historical experience of the utility and for this reason alone, they may be more comfortable implementing a poles and wires upgrade.

- The business case: Developing the business case and cost-benefit for a NWA is more complex than a traditional poles and wires solution. Because the costs of NWAs are not as clear-cut as traditional solutions due to factors like program marketing and customer adoption of technologies, it can be challenging to determine whether they are cost-effective.

- Customer engagement: For a NWA to be successful, load must be reduced. In some cases, there is the potential to defer this load through various demand-side management (DSM) programs. Given the time constraints associated with a T&D upgrade, if the customer incentive levels need to be very high to reach a high penetration level of customer participation in DSM programs in the targeted area, other NWA options can become more cost-effective.

Compounding the difficulties, no standard business models or procurement process exists for utilities to carry out their NWA plans. Four are being considered and under way, however, according to Navigant: request for proposal (RFP), auction, procurement with current implementation contractors, or internal utility resource deployment.

“There is no one right answer for all situations; each case will depend on the utility’s internal structure and capabilities and its regulatory environment,” the report authors point out.

Utility NWA market forecast

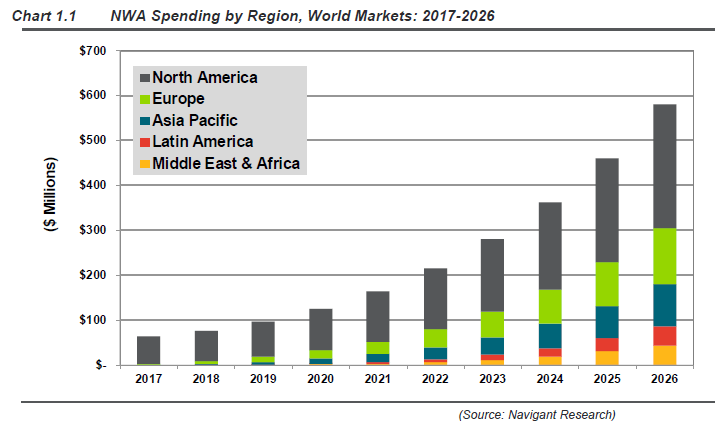

All that said, Navigant Research believes NWA market barriers and obstacles will be surmounted. The market research and consulting company expects some $63 million will be invested in NWA globally this year.

Looking out further, the report authors forecast robust growth in the years ahead as global spending on NWA rises to reach $580 million by 2026. North America, mainly the US, will set the pace, they believe, with regional NWA spending rising to reach $275 million in 10 years.

Improving economics, along with technological improvements and regulatory changes, will be the principal factors driving the surge in use of NWAs, according to Navigant. That includes the costs of purchasing NWA equipment, devices and services, which will fall as economies of scale are approached, as well as deploying and managing the resulting grid-edge and behind-the-meter distributed energy resource and demand response services and products.

According to Navigant: “By far the most significant economic benefit of a NWA is the deferral benefit of the large capital investment. The other benefit streams often account for less than 10 percent of the overall economic benefit.”

*Images credit: 1) NOAA via Wikipedia; 2), 4) Navigant Research; 3) Con Edison

{kind=link}